The Inspector-General of Police, Ag. IGP Kayode Adeolu Egbetokun, PhD, NPM, has assured the general publics of sustained efforts by the Force in tackling crimes and criminality and improved public safety and security across the country. The IGP gave the assurance while charging Commissioners of Police (CPs) in all the States of the Federation and the Federal Capital Territory (FCT), and their supervisory Assistant Inspectors-General of Police (AIGs), to configure the security architecture in their Areas of Responsibility (AoR) for robust and responsive policing ahead of the Eid-el-Kabir celebration which comes up on Wednesday 28th June 2023, to ensure adequate security for the citizenry throughout the festivities and beyond.

According to CSP Olumuyiwa Adejobi, mnipr, mipra, Force Public Relations Officer, Force Headquarters, Abuja in a press release signed on June 27, 2023, the IGP particularly directed the Zonal AIGs and State Command CPs to deploy human and other operational assets to carry out confidence building and crime prevention patrols on major highways, residential and industrial areas, vulnerable points, places of worship, other places of public resort and around all critical national infrastructure devoid of harassment and extortion. The IGP equally warned that personnel deployed must be disciplined, professional, respect the fundamental rights of the citizens, and fulfill their responsibilities with all sense of decorum and alertness.

The Inspector-General of Police, while congratulating Muslim Faithful in the country on the occasion of the year 2023 Eid-el-Kabir celebration, restated that the Force would harness all available assets including relevant groups, associations, sectors, and synergize with other security agencies to boost its service delivery and stabilize general security within the nation.

The IGP wishes all Muslims a happy and peaceful Sallah celebration.

The Federal Inland Revenue Service (FIRS) has partnered with the Market Traders Association of Nigeria (MATAN) to collect and remit Value Added Tax (VAT) to the FIRS from the country’s markets, especially in the informal sector.

According to Johannes Oluwatobi Wojuola Special Assistant to the Executive Chairman, FIRS (Media and Communication) in a press release he signed on June 22, 2023, the Association which has a membership of well over 40 million traders across the country’s 774 local governments, and 36 States plus the Federal Capital Territory is the biggest player in Nigeria’s market space.

The details of the FIRS’ partnership with MATAN was disclosed yesterday at a Stakeholders Engagement Programme on the VAT DIRECT Initiative, held in Lagos State. The partnership will see the FIRS collaborating with the association to deploy technology to enumerate traders for collecting and remitting VAT to the Service, consequently leading to an expansion of the tax net and increased revenue for the Federation.

The VAT DIRECT Initiative (VDI) is a program designed to foster collaboration between the FIRS and the market place, especially the informal sector, in the collection and remittance of the Value Added Tax (VAT) using technology.

Speaking during the Stakeholder Engagement, Mr. Muhammad Nami, Executive Chairman FIRS highlighted that the initiative was the first of its kind, and that it was crucial to revenue generation and also to eliminating multiple taxation, especially from the informal sector.

The Executive Chairman, FIRS who is also the Chairman of the Joint Tax Board (JTB) further stated that the government is worried about the multiplicity of taxes, and that the Service and JTB were working on various modalities of addressing this challenge and that this partnership has laid a very good foundation for the government to address the issue of multiple taxation and extortion by tax officials, tax agents and touts in the market place.

He further noted that the Service would collaborate with security agencies, especially the Nigeria Police, to deal with illegal tax collection by touts in markets.

“One important area of our collaboration is the issue of providing adequate security in the markets. We are aware of the challenges that you have faced in the past with miscreants, self-imposed tax collection agents, and touts.

“I want to assure you that as part of this initiative, we will be collaborating with the relevant security agencies particularly the Nigeria Police Force to tackle all forms of touting and illegal tax collection by miscreants and keep them away from your markets.”

Mr. Nami further noted that the success of this collaboration would lead to increased revenue for the country, and in turn provide government the needed resources to fund infrastructure and other social amenities.

“The successful outcome of this collaboration and additional revenue accruable will have multiplier effects on all sectors of the economy as the government will have more revenue to provide the needed social amenities and infrastructure in critical sectors.

“An improved VAT collection will improve the revenue base of the States and Local Governments at the sub-national level and the citizens will be the ultimate beneficiaries.

“This initiative is very important to the government, particularly at this moment of dwindling revenues from the petroleum sector and therefore, requires that we put all hands on deck and optimally explore all available opportunities.

“The administration of VAT in the informal sector is characterized mainly by a low level of compliance and a lack of awareness in terms of obligation and liability. It, therefore, becomes necessary to leverage the MATAN platform to positively change the status quo,” Mr. Nami stated.

He also noted that to ensure transparency and accountability of the project operations, a combined monitoring and evaluation team comprising both organisations would be formed.

During the Stakeholder Engagement, the Executive Chairman, FIRS also unveiled an Identity Card that is to be given to each trader upon enumeration; the card contains their tax identification number and other personal details.

The VAT Direct Initiative Stakeholder Engagement was attended by the Secretary of the Joint Tax Board, representatives from Deposit Money Banks, Iyalojas of Markets across the country, members of various trade clusters, representatives from all major markets across the country, as well as officers of the Federal Inland Revenue Service.

Royal University of The Kingdom Of Atlantis (RU-KOA) in Singapore has rewarded a Nigerian UNESCO laureate, Prof Sir Bashiru Aremu with three appointments.

The appointment, the school authorities, said was in recognition of his hardwork and dedication towards the improvement of society and humanity.

According to the varsity, the Nigerian-born laureate is to serve as the Vice Chairman Worldwide of RU-KOA in Singapore, the university’s life time fellowship member and chief adviser to the university’s chancellor and chairman of the board, Prof Dr. Michael Puzzolante.

In an executive order signed by Puzzolante as contained in the appointment document, the varsity don said the appointment was in accordance with the institution’s constitution and authority bestowed on him as the University’s Chancellor and chairman of the board.

Puzzolante in the statement stated further that Aremu will be in charge of assisting the chancellor with the promotion of Royal University of The Kingdom Of Atlantis in Singapore Worldwide in order to bring multitude of international students, that Duke Of The Kingdom Of Atlantis will have seat in the University’s Grand Board of Trustees, a development which was implemented on June 24, 2023.

He stated: “In accordance with authorization bestowed in them, the Senate of The Kingdom Of Atlantis in Singapore upon recommendation of the Grand Board of Trustees do confer: Life Time Cértificate of Fellowship to Prof Sir Bashiru Aremu, Fellow of Royal University of The Kingdom Of Atlantis in Singapore”.

“The Fellowship of new scholars and qualified individuals are submitted to the jurisprudence of the Grand Board of Trustees of the RU-KOA Nomination to the rank of scholar is determined based on various criteria and actions presented and observed from the candidate.

“This Fellowship is given with pride and honor to the aforementioned individual for being part of the RU-KOA and contributing to its expansion and for the fire of genius that keeps burning with passion and dedication for the service of the people.”

Aremu, a Professor of computer science, information and communication technology, while reacting to the triple appointments, prestigious awards, honors commended the RU-KOA chancellor, Puzzolante on the gesture and global recognition.

The United Nations Office on Drugs and Crime (UNODC), at a joint press briefing held with the National Drug Law Enforcement Agency (NDLEA) on 19 June 2023, restated its commitment to strengthening efforts in drug prevention, treatment, and control in Nigeria. UNODC Country Representative, Oliver Stolpe, emphasized the importance of international cooperation and addressing the challenges posed by drug trafficking networks.

In a press statement yesterday, Oliver Stolpe outlined the top priorities for UNODC in the coming year. These include:

1. Strengthening International Cooperation: UNODC aims to dismantle trafficking networks involved in the drug trade through enhanced international cooperation with justice systems worldwide.

2. Improving Drug Counseling and Treatment: UNODC will work towards training public and primary healthcare providers to effectively provide drug counseling and intervention. Efforts will focus on increasing the availability of treatment centers and preventing the spread of drug use disorders in Nigeria.

3. Conducting a Drug Use Survey: UNODC will collaborate with the Nigeria Bureau of Statistics to conduct a drug use survey, updating information on drug use and control in Nigeria.

4. School-Based Drug Prevention: UNODC seeks to equip Nigerian children with life skills and knowledge to resist drug use. Existing programs will be expanded to reach a larger number of children, with a special focus on secondary education.

5. World Drug Report: UNODC is eager to learn about the latest developments in the global drug situation. The report will provide insights into the surplus of cocaine production in Latin America, its potential influence on Africa, and issues related to drug use disorder.

The Chairman/Chief Executive Officer of NDLEA, Brig. Gen. Mohammed Buba Marwa (Retd) also disclosed that the fight against substance abuse and illicit drug trafficking has yielded significant results in the last 29 months with the arrest of 31.675 drug offenders; 5,147 of them prosecuted and convicted while over 6.3 million kilograms of assorted drugs were seized within the same period. According to him, ‘This year’s theme, “People First: Stop Stigma and Discrimination, Strengthen Prevention” is in furtherance of the whole-of-society approach to taming the drug scourge. This theme is especially pertinent to the Nigerian situation at the moment. In the past two and the half years, we have strengthened our law enforcement efforts to cut down on the supply of drugs in society.

While charging the society to drop the stigmatization that discourages drug users from seeking treatment, the NDLEA boss expressed appreciation for the partnership between NDLEA, NGOs, development partners, and the various groups, institutions, and relevant professionals in society, including media professionals, who have been very supportive of the renewed war on drugs.” He further thanked UNODC for its “unquantifiable support that has contributed to the rapid evolution of NDLEA” and added “we are thankful to the European Union (EU) and the governments of the United States, United Kingdom, France, India, Germany, who have all boosted our capacity to cope with the demands of our mandate.”

Oliver Stolpe expresses gratitude for the strong collaboration with NDLEA and other Nigerian partners, including NAFDAC, the Federal Ministries of Health and Education, Civil Society Organizations, and the private sector. As the drug epidemic continues to affect millions of people, he stressed the need for all partners to take a people-centered approach to drug policies, with a focus on human rights, compassion, and evidence-based practices. This year’s theme for the World Drug Day is therefore “People First: Stop Stigma and Discrimination, Strengthen Prevention”

Cross River State Governor, Senator Prince Bassey Otu, in further response to the cruise boat accident at the Marina Resort, Calabar, on Saturday, June 24, 2023 involving 14 medical students with three feared dead and 11 rescued, has directed as follows according to a press release e-signed on Sunday 25th of June, 2023 by Emmanuel Ogbeche, Chief Press Secretary to the Executive Governor Cross River State.

That all cruise boat operations and other activities at the Marina Resort be suspended immediately until further notice.

That the cruise boat operators with the management of the State Tourism Bureau are directed to attend a meeting in the Office of the Secretary to the State Government on Tuesday, June 27th, 2023 by 12pm.

“Besides the cruise boat operations, the State Ministry of Transport is to immediately cross-check the safety standards and conditions of all boats operating in the Calabar waterways.

“That the Police should speed up their investigations of the fatal boat accident and prosecute those found culpable to serve as deterrence to others”.

The governor further sympathizes with the families of the affected students over the unfortunate incident.

The Muhammadu Buhari Meteorological Institute of Science and Technology, Katsina (MBMIST) has been granted full accreditation by the National Board for Technical Education (NBTE) to offer National Diploma programmes in Meteorology and Climate Change Science.

This accreditation is contained in a letter signed by Mr Sama’ila Tanko, the Director, Monotechnic Programme Department on behalf of the Executive Secretary of (NBTE) Prof. Idris M. Baguje.

” With reference to the accreditation visitation carried out by the Board to your institution from 10th to 13th May, 2023, I am directed to inform you that the National Board For Technical Education has granted accreditation to the underlisted programmes with effect from 19th May, 2023,” the letter reads.

The accreditation, which is for ND Meteorology and ND Climate Change Science is for two streams of 40 students per programme and is due for another visitation by 2028 upon invitation of the Board by the institute. The MBMIST was founded in 2019 under the leadership of Senator Hadi Sirika , the former Minister of Aviation. It commenced academic activities in the 2020/2021 academic session with in-kind donation of a campus by the Katsina state government through the former executive governor Rt Honourable Aminu Bello Masari and was officially commissioned by Muhammadu Buhari, the immediate past President of the Federal Republic of Nigeria.

The MBMIST which has as it’s motto, Safety, Innovation and Excellence, prides itself as the premier technological tertiary institution for studying Meteorological and Climate Science related programmes, has all the resources for teaching, learning infrastructures, academic curriculum and operations designed to meet with the standards of the World Meteorological Organisation (WMO) and International Standards Organization (ISO). The purpose of the institute is to transform students’ knowledge of weather and climate change science into a love of the subject.

A total of 200 personnel trained in sundry courses graduated yesterday, Friday 23 June 2023, from the Nigerian Air Force Institute of Administrative Management (NAFIAM) Kaduna. The graduates comprised 9 officers and 191 airmen/airwomen, who successfully completed one of the 9 courses organized by the institute. The courses include Initial Personnel Administration Management Officers Course, Integrated Basic Clerical Course, Basic Physical Education Course, Basic Catering Course, Basic Military Band Course, and Basic Information Assistant Certificate Course; all of which lasted for 6 months. Others include the Admin Upgrading A1 Course, Admin Upgrading A2 Course, and Advance Physical Education Course that lasted for 3 months.

Representing the Chief of the Air Staff as the Special Guest of Honour at the occasion, the Director of Administration, Headquarters Nigerian Air Force, Air Vice Marshal Mohammed Yusuf, disclosed the incumbent NAF administration is poised to give adequate priority to training across all specialties with a view to developing robust capacity geared towards effective employment of air power in furtherance of national security. AVM Yusuf, therefore, urged all NAF training institutions to be proactive in their pursuit of capacity development in order to bridge the current skill deficiency across all trades and specialties in the NAF. While congratulating the personnel for the successful completion of their respective courses, the Guest of Honour urged them to exhibit high level of professionalism in discharging their assigned tasks as the course they just concluded has provided them an opportunity to contribute more to the efforts of the NAF in national security.

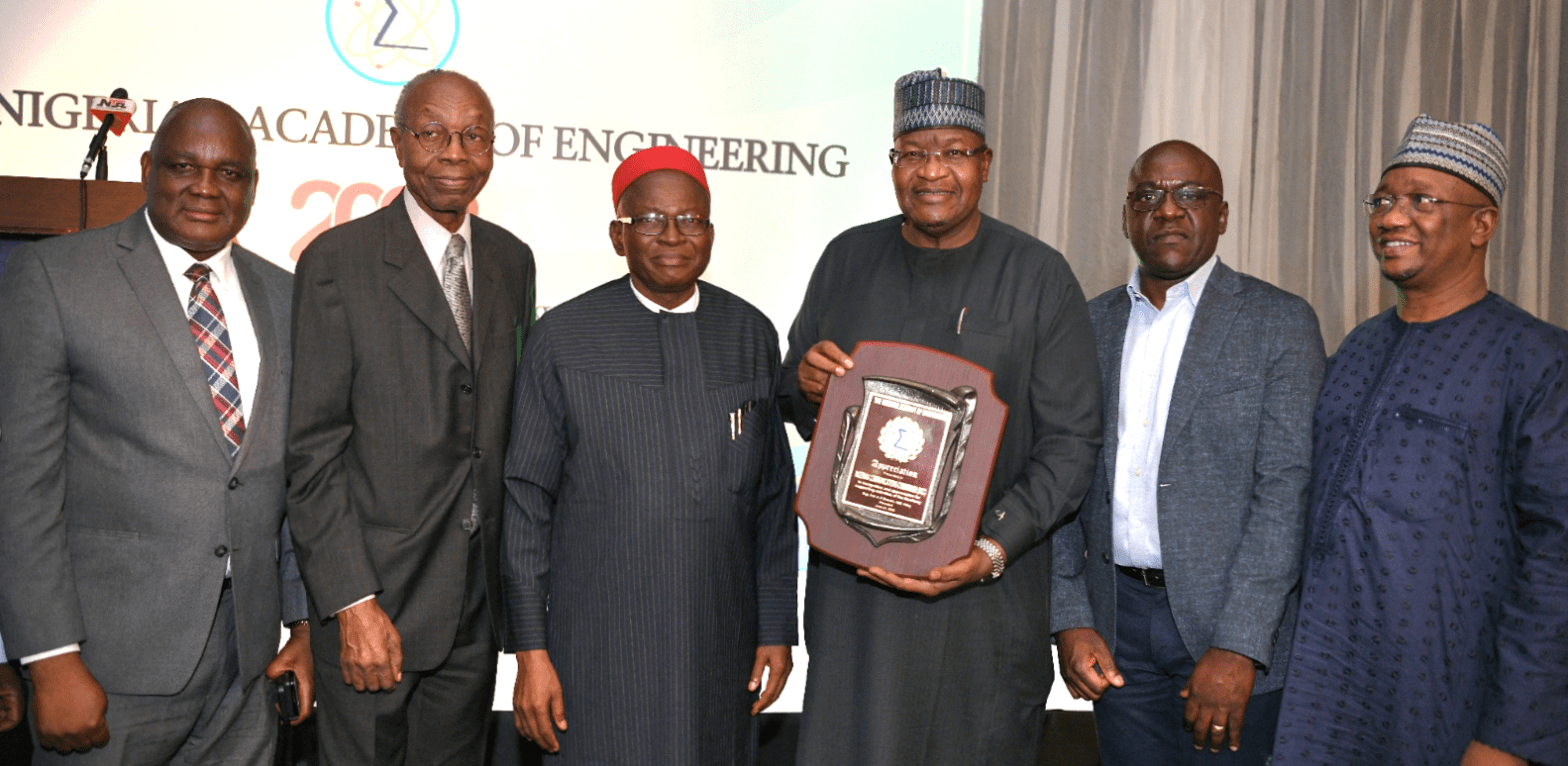

Executive Vice Chairman of the Nigerian Communications Commission, NCC, at the weekend in Lagos, lifted the Platinum Award of the Nigeria Academy of Engineering (NAEng.) being a reward for his leadership of the nation’s telecom regulator for its contributions to the development and growth of engineering profession in the technological and economic development of the country.

According to Reuben Muoka, arpa, fnipr, Director, Public Affairs in a press release he signed on June 25, 2023, stated that President of the Academy, Prof. Azikiwe Onwualu, said during the award presented by doyen of engineering and Former Director General of the Nigerian Television Authority, Vincent Maduka, that the Commission deserved the award as it has done the profession proud in its telecom regulatory process and promotion of engineering as shown in its strong support for the NAEng.

While handing over the award at the 2023 Annual Technology Dinner of the Academy, Maduka said, “Prof. Danbatta has contributed immensely to the sustainability of all initiatives of the professional body, just as his role to the development of engineering profession in general is being felt in Nigeria, through his effective regulation of the telecommunications sector.”

Danbatta, a professor of electrical and electronics engineering, who is a member of Council, and a fellow of NAEng, while receiving the award, expressed appreciation to the illustrious institute for considering the Commission worthy of the award.

Danbatta dedicated the award to the ‘hardworking and diligent staff of the Nigerian Communications Commission’, who, he said, have continued to demonstrate commitment to supporting his vision to promote regulatory excellence toward sustaining growth of Nigeria’s digital economy.

“I could not have done the good work you credited me with, without the support and cooperation of NCC staff and we are delighted that the public is watching, listening and observing what we are doing and a testimony to this fact is the platinum category award we have just been given by the apex engineering body in the country,” the EVC stated.

Danbatta further said: “I want to assure the public that the NCC will do whatever it can, within its mandates, to bring out impactful initiatives that will drive the digital transformation process that will ultimately make telecom services pervasive and affordable to all parts of the country.”

He used the opportunity to speak about some of the initiatives of the Commission that have struck a rhythm in the socio-economic development of the nation.

These, he said, include the one targeted at the Nigerian youths across the country where the Commission trains the youth, provides them with laptops, and other equipment that can make them access the internet with a view to equipping them to develop their skill and earn a living.

Danbatta assured of the Commission’s commitment to driving digital connectivity aimed at bridging extant clusters of access gaps in Nigeria. “We have a target of 70 per cent broadband penetration by 2025, as contained in the Nigerian National Broadband Plan (NNBP). We are around 50 per cent currently and I can assure you that we are hopeful that we will achieve and surpass that target,” he said.

The Nigerian Academy of Engineering was established to pursue excellence in science, technology and engineering as well as provide a national platform for experts to harness their experiences and insights and make input into public and private technical policy.

As part of its efforts to promote stability in areas affected by Boko Haram, the Multinational Joint Task Force (MNJTF) has handed over a block of three classrooms, a staff office and four boreholes to the inhabitants of Toumour in Diffa Region, Niger Republic. The handing over was held on Wednesday 21 June 2023. The project was facilitated by the European Union through the COGINTA Non Governmental Organisation.

According to Lieutenant Colonel Abubakar Abdullahi, Chief of Military Public Information in a press release release he signed on the 22 June 2023, stated that while handing over the projects, the Force Commander, Major General Gold Chibuisi represented by Colonel Bamouss Ngarsara, Chief of Administration MNJTF expressed gratitude to the people of Toumour for their warm reception and contribution to the return of peace and security in their communities. He highlighted the importance of education as a tool for transforming communities and building lasting peace. He further commended the efforts of COGINTA and the European Union for their direct support in promoting stability in the region.

The Governor of Diffa region Smaïne Younouss represented by his Secretary General, Barde Dauda in his response, lauded the MNJTF for working tirelessly to restore peace and security in the communities affected by Boko Haram. He expressed the commitment of the local authorities to work more closely with the MNJTF and other development partners in promoting socio-economic development in the region.

The block of classrooms and staff offices handed over will provide an enabling environment for the education of children and young people in the locality while the boreholes will help to alleviate the water shortage in the area and improve the living conditions of the people. The projects are part of the MNJTF’s Civil-Military Activities (CIMIC) and will help to strengthen the relationship between the military and civilian populations in the region recovering from Boko Haram crisis.

The handover ceremony was attended by local authorities, community leaders, and representatives of development partners. It symbolizes the commitment of the MNJTF and its partners to promoting peace, stability, and development in the areas affected by Boko Haram. The MNJTF is working closely with other stakeholders to restore normalcy in the region and provide the necessary support for the humanitarian and development needs of the affected communities.

As the risks facing our natural world increases by the day, environmentalists are always looking for new ways to tackle issues such as flooding, deforestation, climate change, and carbon emissions. Whilst many organizations are busy rallying volunteers to bang the drum for the environment, there is perhaps an unsung hero patiently waiting on the sidelines – the mangrove tree. Planting mangroves has been proven to help with environmental issues.

Mangroves are magical. Planting more of them could help restore the health of the planet’s lands, seas, and climate.

It is against this backdrop Compassionate Advocacy For The Poor Initiative, CAPI, in collaboration with the Ministry of Environment, Bayelsa State embarked on a two days mangrove planting exercise in Opume Kingdom to curb future flooding in the State.

The event which commenced on the 9th to 10th June 2023 is aimed at enhancing living on land as one of CAPI’s aims and objectives is to protect the former and serve as a frontline defense for the people and property along the coasts.

While declaring the event open in Bayelsa State, the founder and Executive Director, of Compassionate Advocacy For The Poor Initiative, CAPI, Dr. Edet Umoh, stressed the need for the help the federal government and international organizations to come to the aid of Bayelsa State statistically stating that over 1.3 million people have been displaced over the years.

The first day which was characterized by community engagement activities, and stakeholder dialogues on a series of topics around flooding mitigation exposed lots of challenges the Bayelsa state indigenous people are going through and lots of lives and properties lost over the years.

Also speaking, the Director Climate Change/ Programs, CAPI, Rukaiya Mahmoud, has this to say, “The black mangrove is a species of tree that can typically be found growing in coastal areas. It is characterized by its dark leaves and deep, knotted roots, which help anchor it firmly in the muddy soil of tidal flats and mangrove swamps.

“But why is this tree so important? Well, for one thing, black mangroves provide vital habitats for many different types of animals. Fish, birds, and other wildlife rely on the shelter of mangrove forests to survive, and many species use the trees as nesting sites, feeding grounds, and breeding areas.

“But the benefits of black mangroves go beyond just providing homes for animals. These trees play a crucial role in reducing coastal erosion and protecting against storm surges and other natural disasters. They also help to filter and purify the water in which they grow, removing pollutants and other harmful substances.

“In addition, mangroves are known to sequester large quantities of carbon, making them a valuable tool in the fight against climate change. By capturing and storing carbon dioxide from the atmosphere, mangroves help to reduce greenhouse gas emissions and slow down global warming.

‘Unfortunately, black mangroves and other species of mangrove trees are under threat from a variety of human activities, including deforestation, pollution, and development. As we continue to expand and encroach upon these fragile ecosystems, we risk irreparably damaging some of the most important ecosystems on the planet.

“That’s why we must take steps to protect and preserve these vital ecosystems. We must work to reduce our carbon footprint, prevent pollution, and promote sustainable development that balances the needs of people and the environment.

“So let us remember the important role that black mangroves and other mangrove species play in supporting life on our planet. And let us commit ourselves to doing all that we can to protect and preserve these precious habitats for future generations”.

The representative of the Ministry of Environment, Mr. Wakedei Davidson Ere, Director of Climate Change hampered on the need for stakeholders engagement stating that it is essential for success in any sphere of life. “By involving all parties affected by decisions, we build trust, foster transparency, and improve outcomes. A structured approach that regularly checks in with stakeholders is essential, and we must commit to ongoing collaboration to achieve common goals”, he said.

The 2nd day which was Mangrove planting witnessed a lot of participants including community leaders out of which were Festus Egba Director of Forestry, Ministry of Environment, Bayelsa State, Diete-Spiff Michael O., Director, Mitigation, Ministry of Environment, Bayelsa State, Frank Azibaobeh, CAPI staff, Susan Enemughan, Asst Director, Forestry, Ministry of Environment, Bayelsa State amongst many others.